by

Michael Noreman, CPA, MST, MAcc, Alvarez & Marsal Tax, LLC

| March 26, 2024

In today’s work environment, the prevalence of hybrid teams has steadily risen. For CPAs, managing a team that seamlessly blends in-office and remote work has unique challenges and opportunities. As the accounting profession evolves, so must the leadership strategies employed by CPAs to foster collaboration, maintain productivity and ensure the well-being of their teams.

The Rise of Hybrid Teams in the Public Accounting World

The accounting profession has traditionally been office-centric, with CPAs collaborating in person in the office or at a client site. However, the advent of more advanced audio and video conferencing software, coupled with global events such as the COVID-19 pandemic, has reshaped the way firms operate. Hybrid teams — a blend of in-office and remote workers — have become a necessity for firms aiming to adapt to the evolving demands of the profession.

Embracing Technology for Seamless Collaboration

In a hybrid team environment, technology is the anchor that holds everything together. Firms need to invest in robust communication and collaboration tools that facilitate seamless interaction among team members, regardless of their physical location. Cloud-based software, video conferencing platforms and project management tools have become essential components of a CPA firm’s digital infrastructure.

Providing comprehensive training on these tools is crucial to ensure that all team members, whether in the office or working remotely, are proficient in using the technology. This not only enhances collaboration but also ensures that everyone is on the same page when it comes to adopting best practices in workflows.

Fostering a Culture of Inclusivity and Communication

One of the primary challenges in leading hybrid teams is maintaining a sense of unity and camaraderie among team members who may be geographically dispersed. Firms need to foster a culture that values open communication and inclusivity. Regular team meetings, both virtual and in-person, help build personal connections and ensure that everyone is aligned with the firm’s goals.

Leaders should actively encourage team members to share their thoughts, ideas and concerns. This creates an environment where everyone feels heard.

On days when the team gathers in person, engaging in team-building events can prove invaluable, fostering positive camaraderie and significantly boosting morale. Something as simple as a team coffee break or a lunch can go a long way in encouraging connection, building personal relationships and developing professional trust.

Flexibility and Work-Life Balance

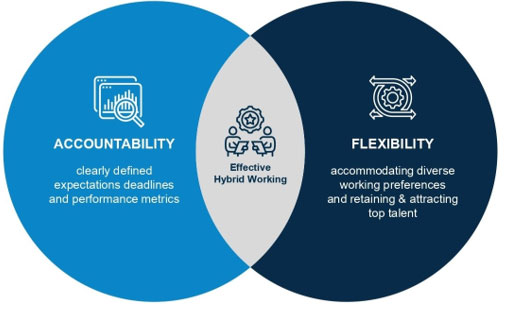

Hybrid teams offer the advantage of flexibility, allowing firms to attract and retain top talent by accommodating diverse working preferences. However, it is essential for leaders to strike a balance between flexibility and accountability. Clearly defined expectations, deadlines and performance metrics ensure that all team members, whether working in the office or remotely, contribute to the firm’s success.

Strategic Presence

Mastering the art of knowing when to be in the office versus working remotely becomes a critical aspect of effective leadership in a hybrid environment. For professionals in public accounting, where relationships and networking are paramount, discerning the appropriate times to be physically present in the office is crucial. While the flexibility of remote work offers undeniable advantages, there are instances where being in the office facilitates spontaneous interactions, collaboration and networking opportunities that are integral to the profession. Striking the right balance involves a nuanced understanding of the demands of public accounting, ensuring that team members are strategically present when face-to-face engagements and networking are essential.